Two years into starting my own practice, it still takes me an absurd amount of time to write a well thought out blog post (which is why I rarely) do it, but since I’m supposed to have at least some content on my website, I’m going to try the exact opposite of well thought-out.

How does 3am ramblings sound?

If my wife and I forget to put our sound machine on, 3am is the time we’ll wake up after someone with a tuned exhaust races down our street (unclear why they don’t take Dufferin instead), or more recently, it’s the time our newborn decides to feast, poop, or some loud combination of the two.

It’s about the time I’m unable to fall back asleep and will occasionally think about exciting things like, who has the best takeout sandwich in the Parkdale/Roncy/Brockton/Junction area, and the American love affair with Drake.

The mind also drifts back to the Investment Plans I do for clients, what they’re investing in and the conversations I have with them. After 2 years, my analyst training has me looking for trends, trying to eliminate outliers and just trying to come up with a picture that is not 100% right, but hopefully, a bit less wrong.

So, what ARE they investing in? Here are some not well thought-out observations which are probably going to sound like 3am ramblings. They are.

1.) There are still plenty of shitty mutual funds out there. Shitty shit shit. And It’s the usual suspects overcharging people without them knowing, but at least they’re pretending to actively manage their pot, bravo!

2.) In a weird twist, one of the alternatives showing up are overpriced portfolios of index funds. I think the sales pitch is “hey, we’re looking out for you, we can save you money on fees by investing in index funds”. Except that a passive portfolio for almost 0.70% isn’t that great either. I’ve also seen some “independent” advisors tack on a 1% fee on top of that, I guess as comp for their twice per year calls? Their pitch is the same - going from an actively managed fund at 2.4% to a passively managed portfolio for 1.7% is a win for YOU the consumer. **eye-roll emojii**

3.) I’m not thrilled with Robos. They fall into the above criticism of index funds, which many times, ends up being an expensive indexed portfolio. There are excellent Canadian investment managers out there who charge not much more, for true active management. Those are more attractive options, in my opinion, OR if you want to go true passive, Vanguard and Blackrock both offer diversified ETF options and at this rate, those investment products will be free if they keep up their price war.

4.) The Non-bank Discount brokerages got game. I was wrong in thinking I’d see DIY Investors go to their bank’s own online broker (like TD Waterhouse). Instead, clients seem to be ditching the bank altogether. Maybe the bank didn’t tell them there was an online broker option? In the meantime, it’s been over a decade since the E-trade baby told us that investing was simple, not to be outdone by Questrade’s anger-inducing campaign https://www.youtube.com/watch?v=zyFyRQSaSEI&list=PL4E3463842B01E133

5.) Re-focusing a person’s individual investment objectives and really figuring out the goal of their investments gets totally overlooked by the sales machines out there. A lot of clients in are stressed because they’re comparing their investments to unrealistic expectations or expectations that aren’t relevant TO THEM.

6.) Back to Robos for a second. They do generate the most inquiries from people. By they, I mean WealthSimple and that’s not to put down the other Robos out there, but it certainly feels like WealthSimple and the 7 dwarfs in Canada. Mostly because they throw an insane amount of money on advertising, which btw, is probably the best financial services branding/marketing in the country. That said, you the client, is paying for those slick spots during the Jays game.

7.) ETF’s scare people. Partly because we’ve at least heard about mutual funds for forever, whereas ETF’s seem like something new and exotic by comparison. Yes, many clients feel like ETF’s are exotic. But I think the bigger issue is mental responsibility for one’s own investment performance. No one wants it. Even with the simplicity of all-in-one ETF’s, https://www.youandyoursfinancial.com/insights-and-advice/2018/5/17/etf-autopilot

8.) Since this post is clearly coming across as if I dislike everything, some good news! Financial literacy IS getting better!!! People are becoming more engaged and asking more questions compared to when I first started. But….financial literacy in Canada, generally, is total shit.

But it’s getting better….

…..in my totally self-selecting client world.

On to some petty things

9.) The retirement I think most people are looking for comes by way of a workplace pension (in addition to CPP) and zero-mortgage combo. I still see these. They make me happy. I’m worried I’ll see less. I’ve stopped worrying about young people. Many will need to find their own way. At least they have time and technology.

9b.) Just a reminder that CPP will be around. At some point you may have to work longer to get it. You’ll most definitely have to pay more into it. But it will be around.

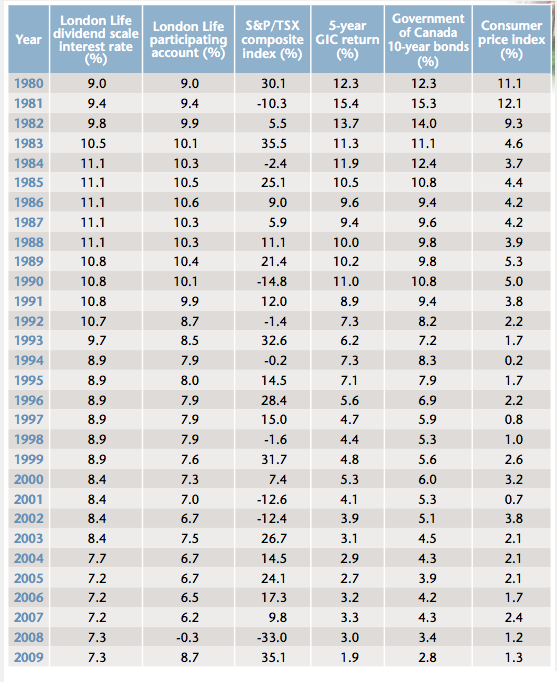

10.) There’s no need to bash bonds. Everyone said they rates were headed higher in 2010. And 2011. And 2013. And 2015. And 2018. They serve a purpose and no one can predict the future

11.) My vibe is that Downsizing is a myth. Getting any significant amount of home equity to fund retirement will mean (for most people) leaving the area they’re in, moving into a place far smaller than their expectations or, hopping on the reverse mortgage train, which is one of my least favourite products, but admittedly, I think will be an incredible source of growth for financial institutions over the next few decades.

12.) Comparing investment options exclusively based on fees is not a productive exercise. I probably should have said this way up top when I started talking about fees.

There’s a lot of shelf space on the internet and a place for active management, robos and passive. Part of the fun with this job is figuring out which of those options provides the most value to an individual or family.

And having the flexibility to say so.

Good morning.